WEBINAR REPLAY: 2025 Open Enrollment Info

If you missed our 2025 Individual Health...

WEBINAR REPLAY: 2024 Open Enrollment Info

If you missed our 2024 Individual Health...

WEBINAR REPLAY: 2023 Open Enrollment Info

If you missed our 2023 Individual Health...

2022 Open Enrollment: Record-low Premiums Available

The 2022 Open Enrollment period began on...

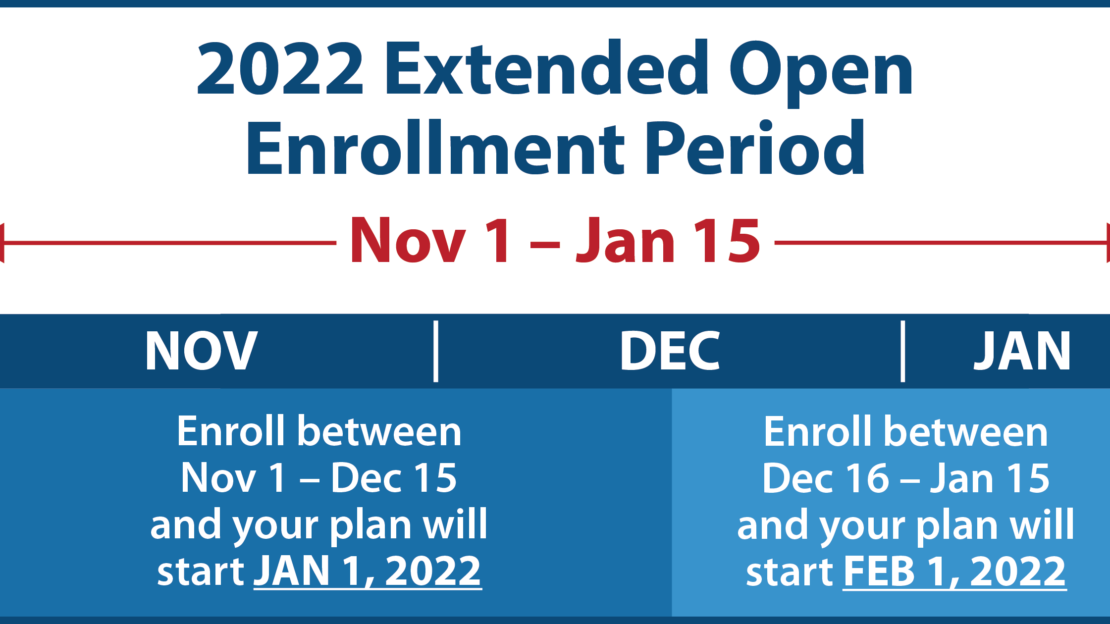

2022 Open Enrollment Period: Important Dates

The annual Open Enrollment period for in...

WEBINAR REPLAY: 2022 Open Enrollment Info

If you missed our 2022 Individual Health...

The 2021 COVID-19 Special Enrollment Period: Final Week

While health insurance enrollment is typ...

The 2021 COVID-19 Special Enrollment Period: What You Need To Know

On Thursday, January 28, 2021, President...

5 Ways to Help You Stay Healthy This Holiday Season

The holidays are going to look a lot dif...